Welcome to the fifth and final lesson in Interest, Savings, and Borrowing! Over the course of this unit, we have built a solid toolkit: reading interest terms, computing single-period interest, calculating simple interest across multiple periods, and most recently, working through compound interest year by year. Each lesson added a new layer, and now it is time to bring both methods together for a head-to-head comparison.

In this lesson, we will place simple and compound interest side by side using the same principal, rate, and time. We will calculate the ending balance for each method, measure the dollar difference between them, and explore why compounding produces larger growth the longer we wait.

Simple and compound interest share the same three inputs — principal (), rate (), and time ( periods) — yet they handle the base differently. Simple interest sticks with the original principal every period, while compound interest folds each period's earned interest into the balance so the base grows.

When there is only one period, both methods give the exact same result. The real question is: how much more does compounding earn when we stretch the time to several years or beyond? The rest of this lesson answers that question with concrete numbers.

Let's line up both methods with a familiar set of numbers: $1,000 at 10% annual interest for 3 years.

With simple interest, each year adds the same flat amount: $1,000 × 0.10 = $100. With compound interest, each year's interest is calculated on the updated balance, as we practiced in the previous lesson. Here is how the two paths compare:

At the end of Year 1, both methods produce exactly $1,100. By Year 3, compound interest has reached $1,331 while simple interest sits at $1,300. The compound method earned $31 more, entirely from interest accumulating on previously earned interest.

The gap between the two methods comes down to what serves as the interest base each year. With simple interest, only the original $1,000 ever earns interest, so we get a flat $100 every year. With compound interest, the base grows because prior interest is included. Let's trace the per-year interest for each method:

- Year 1: Both earn $1,000 × 0.10 = $100. Gap: $0.

- Year 2: Simple earns $100 again. Compound earns $1,100 × 0.10 = $110. The extra $10 is interest on Year 1's $100. Cumulative gap: $10.

- Year 3: Simple earns $100. Compound earns $1,210 × 0.10 = $121. Cumulative gap: $31.

Each year, the compound base is larger, so it generates more interest than the year before. The difference starts at zero and grows with every additional period.

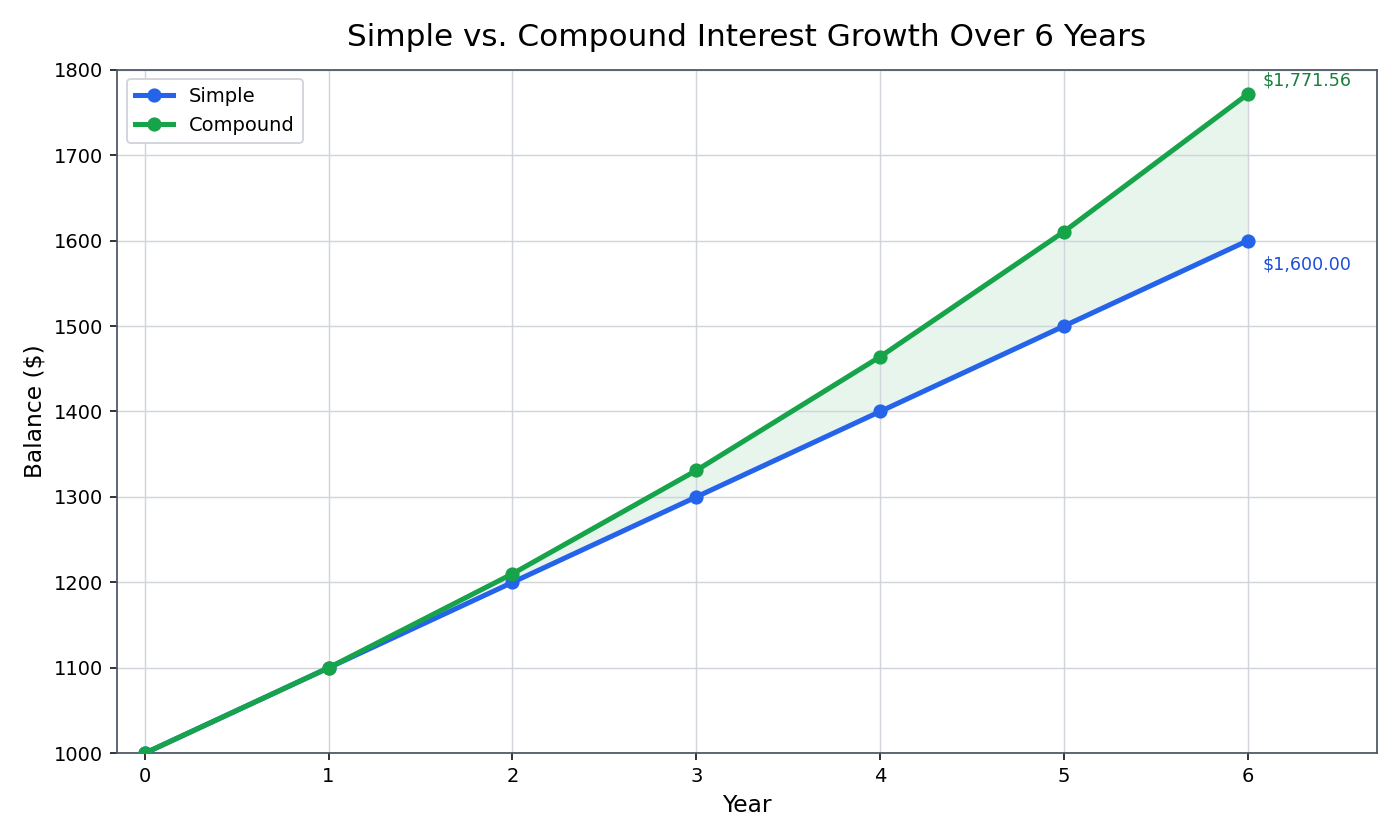

The extra earnings from compounding do not increase at a steady pace — they speed up. To see this clearly, let's extend our $1,000 at 10% example to 6 years and track the dollar difference:

Look at the Difference column. It jumps from $10 after Year 2 to over $171 after Year 6. Simple interest adds the same flat $100 each year, producing a straight-line growth pattern. Compound interest adds a larger amount each year because the base keeps growing, creating a curve that pulls further and further ahead. The longer the time horizon, the wider this gap becomes.

A graph makes this widening gap easier to see:

Let's put this insight to work with a more realistic scenario. Imagine we deposit $5,000 at 5% annual interest for 10 years and want to compare the two methods.

Simple interest gives us a direct calculation using the formula from Lesson 3:

In this lesson, we compared simple and compound interest side by side and confirmed that compounding always produces a larger ending balance when the time horizon is more than one period. The key reason is that compound interest uses a growing base, so each period generates a bit more interest than the last. The longer the time frame, the more this "interest on interest" effect stacks up, and the wider the dollar gap becomes.

This wraps up the lessons in Interest, Savings, and Borrowing. In the upcoming exercises, you will decide which method wins in various scenarios, complete comparison tables, calculate exact dollar differences, and write your own explanation of why compounding pulls ahead over the long run. Let's finish this course on a high note!