Welcome to Lesson 4 of 5 in Interest, Savings, and Borrowing — we are nearly at the finish line! So far, we have built up from reading interest terms to computing single-period interest and then extending that work across multiple periods with simple interest. In every calculation up to this point, the base stayed locked at the original principal.

This lesson changes the game. We will explore compound interest, where each period's interest is added to the balance before the next calculation begins. Instead of a fixed base, the base grows from one period to the next. We will work through this process year by year, building each new balance step by step.

With simple interest, the base never moves — it is always the original deposit or loan amount. Compound interest takes a different approach. At the end of each period, the interest earned is folded into the balance, and that updated balance becomes the base for the following period.

Think of it like a snowball rolling downhill. Each rotation picks up a bit more snow, which makes the ball bigger, which means the next rotation picks up even more. With compound interest, each period's interest is a little larger than the last because the base itself has grown. This "interest on interest" effect is what makes compounding powerful over time.

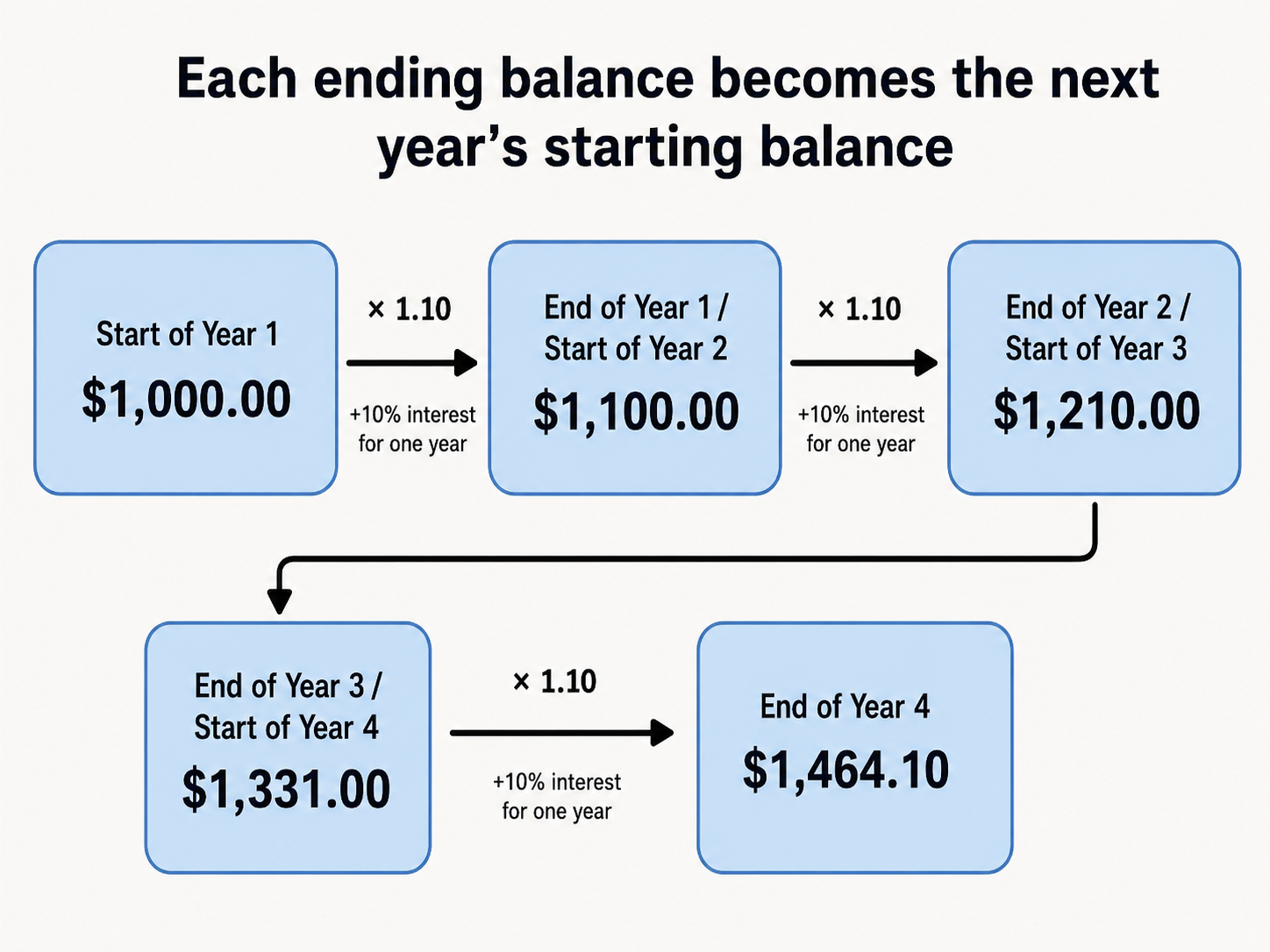

Let's trace through a concrete example. Suppose we deposit $1,000 into a savings account that pays 10% annual interest, compounded yearly. We want to find the balance at the end of each year.

Year 1 looks exactly like a single-period calculation. We multiply the principal by the rate:

The new balance at the end of Year 1 is:

Here is where compounding parts ways with simple interest. Instead of going back to the original $1,000, we use the end-of-Year-1 balance of $1,100 as the base for Year 2:

Let's continue the same example through 4 years so we can watch the pattern unfold. Each row uses the previous row's ending balance as the new base.

(All values shown in dollars.)

Each year, the interest is a little larger because the base has grown. After 4 years the balance is $1,464.10. Under simple interest with the same principal and rate, it would be $1,000 + ($1,000 × 0.10 × 4) = $1,400. Compounding earned an extra $64.10 in this scenario.

The flow diagram below makes the handoff from one year to the next easier to see:

Every row in the table above follows the same two-step process:

- Calculate interest: Multiply the current balance by the rate.

- Update the balance: Add the interest to the current balance to get the new starting point.

We can express both steps at once. If we call the balance at the start of a period , the balance at the end of that period is:

Let's try a more practical scenario. Suppose we open a savings account with $2,500 at 4% annual interest, compounded yearly, and leave it untouched for 3 years.

Our multiplier is . We apply it once per year:

(All values shown in dollars.)

After 3 years the balance is $2,812.16. The total interest earned is $2,812.16 − $2,500.00 = $312.16. With simple interest, the total would have been $2,500 × 0.04 × 3 = $300.00. Compounding added an extra $12.16 over just three years — and as the number of periods grows, so does this gap.

As you begin practicing these calculations, a few specific errors come up often. Keeping them in mind will save you time and frustration:

- Using the original principal every year. That produces simple interest, not compound. Always carry the updated balance forward as the base for the next period.

- Rounding too early. When an ending balance includes cents, carry the full amount into the next year's calculation. Round only when reporting a final answer.

- Skipping the order of operations. Calculate interest first, then add it to the current balance, then move to the next year. Mixing up or skipping a step will throw off every row that follows.

In this lesson, we learned that compound interest works by adding each period's interest to the balance before calculating the next period. The result is a growing base that produces slightly more interest with every cycle. The key technique is to multiply the current balance by for each period and use that result as the starting balance for the next one.

Now it is time to put this iterative process into action. In the upcoming exercises, you will fill in year-by-year tables, compute compound balances for different principal-and-rate pairs, and explain in your own words why the base changes from period to period. Let's get that snowball rolling!