Welcome back to Multi-Step Percent Problems! This is the fifth and final lesson of the course, which means you have worked through every major building block: choosing the correct base, recovering an original amount, applying consecutive percent changes, and mixing percent adjustments with fixed-dollar amounts. That is an impressive run, and you are about to tie it all together.

In everyday life, we rarely face just one offer in isolation. Instead, we are asked to choose: Which deal saves the most money? Which plan costs less over a year? Which payment option gets us ahead faster? Each choice typically involves its own chain of percent and dollar steps, and the winner is not always the one that "looks" better at first glance. In this lesson, we will learn a reliable method for calculating the final result of two competing multi-step options and selecting the one that best meets a stated goal.

Before we jump into numbers, let's frame the strategy. As you have seen throughout this course, every multi-step percent problem boils down to performing each adjustment in the correct order on the correct base. Comparing two options simply means doing that process twice — once for each option — and then placing the two final results side by side.

The critical habit is to finish all the math before you judge. A 30% discount sounds bigger than 20% off plus a $15 coupon, but whether it actually saves more money depends on the starting price and the order of steps. Our job is to let the numbers decide, not our first impression. This "calculate, then compare" mindset will guide every example in this lesson.

Let's start with a straightforward shopping example.

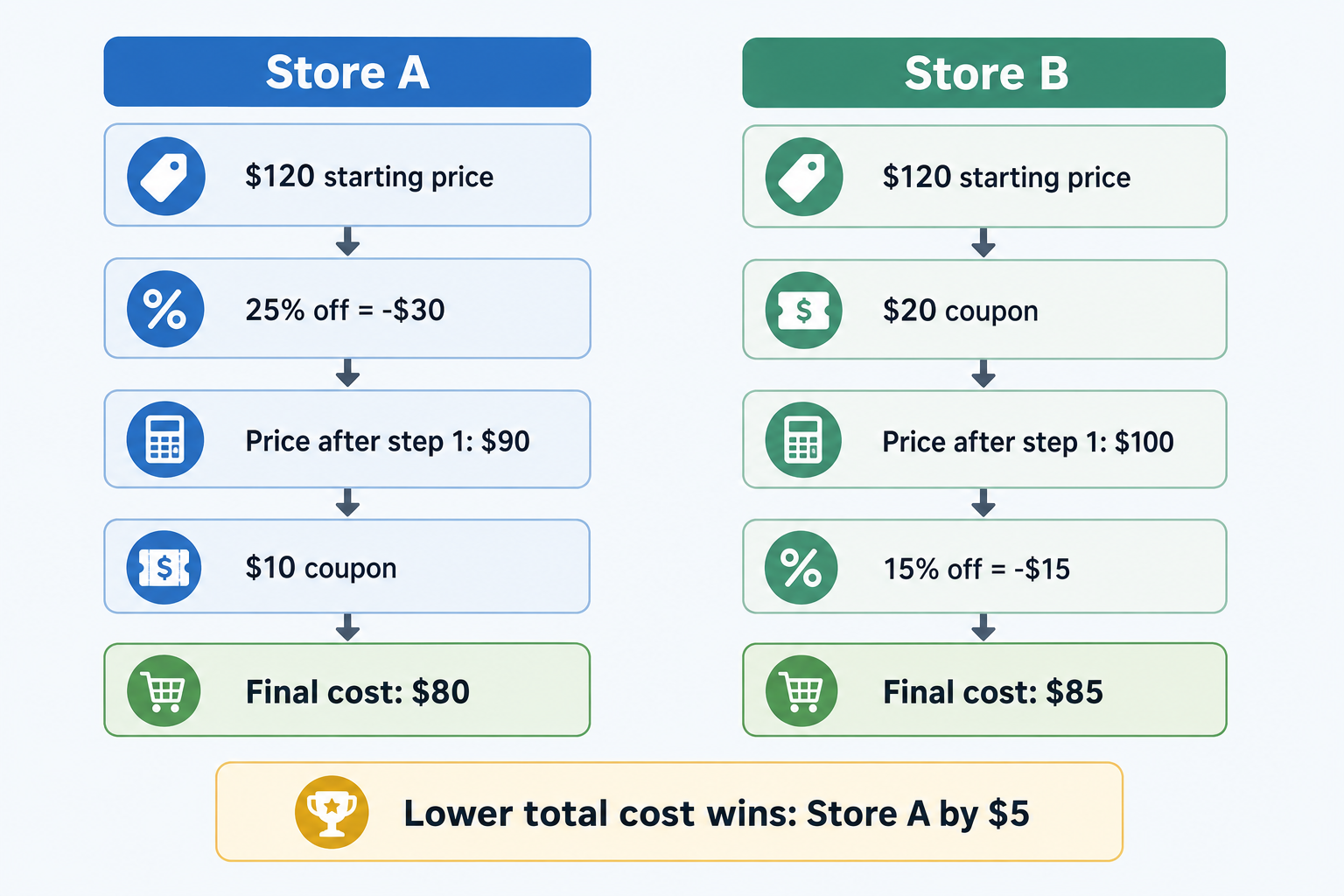

Scenario. A pair of headphones is priced at $120. Two stores sell the same item:

- Store A: 25% off, then a $10 coupon applied to the reduced price.

- Store B: $20 coupon first, then 15% off the remaining balance.

Our goal is the lowest total cost.

For Store A, the percent step comes first. The discount is 120 × 0.25 = $30, bringing the price to 120 − 30 = $90. Then the $10 coupon is subtracted: 90 − 10 = $80.

For Store B, the fixed-dollar step comes first. Subtracting the $20 coupon gives 120 − 20 = $100. Then the 15% discount is 100 × 0.15 = $15 off, so the final price is 100 − 15 = $85.

Store A wins by $5. Notice that Store B's 15% discount is applied to a smaller base ($100 instead of $120), which limits its impact. This is exactly why running both calculations is essential — the larger-sounding percent does not always produce the bigger savings.

Sometimes both options involve only percent-based adjustments, but in different combinations. Let's look at a scenario like that.

Scenario. A $200 winter coat is available through two promotions:

- Promo X: 30% off, then an additional 10% off the sale price.

- Promo Y: A single 35% discount applied once.

For Promo X, we chain the two percent changes:

Multi-step percent comparisons are especially useful for subscriptions, memberships, and payment plans. Let's walk through a slightly larger example.

Scenario. You are choosing between two annual gym memberships. The standard monthly rate is $50.

- Plan A: Pay monthly at full price for 12 months, but receive a 10% loyalty discount on the last 6 months.

- Plan B: Pay upfront for the year at a flat 8% discount on the entire annual cost.

Our goal is the lowest annual cost.

For Plan A, the first 6 months are at full price: 50 × 6 = $300. The remaining 6 months get a 10% discount, so each month costs 50 × 0.90 = $45, and those 6 months total 45 × 6 = $270. The annual cost is 300 + 270 = $570.

For Plan B, the full annual cost would be 50 × 12 = $600. An 8% discount on that amount gives 600 × 0.08 = $48 off, so the annual cost is 600 − 48 = $552.

Plan B saves $18 more per year, even though its discount rate (8%) appears lower than Plan A's (10%). The difference is that Plan B's 8% applies to the entire year, while Plan A's 10% only covers half the year. This is a great reminder that the base a percent applies to matters just as much as the percent itself.

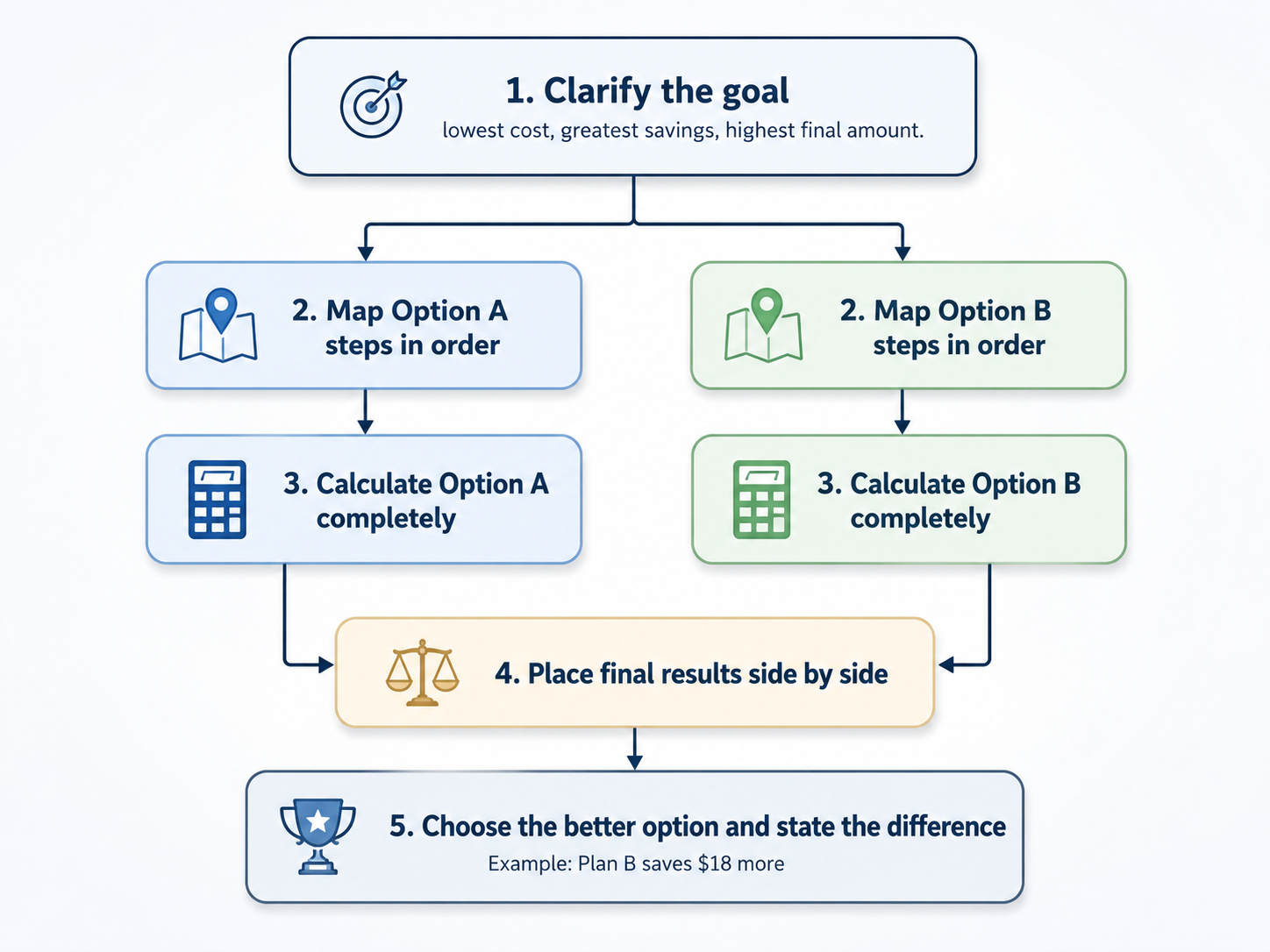

Across all the examples above, we followed the same pattern. Here is a compact framework you can use every time you face competing offers:

- Clarify the goal. Know whether you want the lowest cost, greatest savings, highest final amount, or something else.

- Map each option's steps. Write down the adjustments in order, noting which are percent-based and which are fixed amounts.

- Calculate each option separately. Apply every step to the correct base, just as we practiced in earlier lessons.

- Place the final results side by side. Compare the two numbers against the stated goal.

- State your choice and the difference. Saying "Plan B saves $18 more" is always stronger than just naming the winner.

This framework works whether you are comparing store deals, subscription plans, or loan payoff strategies. The math tools are the same ones you have been building all course long.

Two traps appear frequently when comparing options:

- Judging by the percent alone. A higher percent discount is not automatically better. As the gym membership example showed, the base that percent applies to and the portion of the total it covers can completely change the outcome. Always compute the final number.

- Forgetting a step in one option. When juggling two multi-step calculations at once, it is easy to skip a fee or tax in one of them. Writing both options out in a labeled table or list keeps the work organized and complete.

A quick sanity check at the end also helps: ask yourself whether each final amount is reasonable given the starting price and the size of the discounts or fees involved. If a 10% discount somehow cut the price in half, something went wrong.

You now know how to compare two multi-step percent options by calculating each one fully and then measuring the results against a clear goal. The key insight is simple but powerful: appearances can mislead, so we let the arithmetic decide. Combined with everything else you have practiced in this course — choosing the right base, reversing a percent change, chaining consecutive percent adjustments, and mixing percents with fixed amounts — you have a complete toolkit for tackling layered percent problems in real life.

Up next, you will put this comparison skill to the test with hands-on exercises. You will fill in side-by-side setups, compute totals for competing offers, and write a recommendation for a realistic personal-finance decision — this is your chance to show everything you have learned!