Welcome to Interest, Savings, and Borrowing, the third course in our learning path! In the first two courses, we built a solid foundation with percentages and applied them to shopping scenarios like discounts, tax, and tips. Now we are stepping into the world of personal finance, where percentages play an even bigger role because they determine how much money grows in a savings account or how much a loan truly costs.

In this first lesson, we will learn how to read and identify the three key pieces of information that appear in nearly every savings or loan statement: the principal, the rate, and the time period. We will also make sure we can explain in plain language what an interest rate actually means. These building blocks will set us up for all the calculations ahead.

As you may recall from previous courses, a percent tells us a portion "out of 100." When a store says "20% off," it means 20 out of every 100 dollars is removed from the price. Banks and lenders use percentages in a similar way, but instead of taking money away, they describe how much extra money is added over time.

That extra money is called interest. If you put money into a savings account, the bank pays you interest as a reward for keeping your money there. If you borrow money through a loan or credit card, the lender charges you interest as the cost of borrowing.

In both cases, the interest amount depends on three things: how much money is involved, what percentage is applied, and how long the arrangement lasts. Let's look at each one.

Every interest statement, whether it comes from a bank, a car dealership, or a credit card company, contains the same three pieces:

Think of these three components as the "who, how much, and how long" of any interest situation. The principal is the money involved, the rate is the percentage applied each period, and the time period is the duration over which interest accumulates. Now let's explore each component in more detail so you can confidently spot them in any financial statement.

The principal is simply the original amount of money before any interest is added. In a savings account, it is the amount you deposit. In a loan, it is the amount you borrow.

For example, consider this statement:

"You are approved for a car loan of $18,000 at 5% per year for 4 years."

Here the principal is $18,000 because that is the starting amount being borrowed. A quick way to spot the principal is to look for a dollar amount that is described as a deposit, a balance, or a loan amount. It is always a dollar figure, never a percentage.

The rate (also called the interest rate) is the percent that gets applied to the principal during each time period. In the same car loan example above, the rate is 5% per year. Notice that a rate always has two parts:

- A percent value (like 5%)

- A time frame it applies to (like "per year" or "per month")

This pairing matters. A rate of 5% per year is very different from 5% per month. When a statement says "APR," that stands for Annual Percentage Rate, meaning the rate applies on a yearly basis. Credit cards often show a monthly rate as well, sometimes labeled "monthly periodic rate." Always check which period the rate refers to.

The time period (often called the term) tells us how long the interest arrangement lasts. In our car loan example, the time period is 4 years.

Time periods can be stated in years, months, or even days depending on the product. A mortgage might have a term of 30 years, a certificate of deposit might mature in 18 months, and a short-term personal loan might last 90 days. The important thing is to note the unit (years, months, days) so that later, when we calculate interest, the time unit matches the rate's unit.

Now that we can identify the three components, let's make sure we can explain an interest rate in everyday language. When a bank says your savings account earns 2% per year, it means:

For every $100 you keep in the account for one year, you earn $2.

That is the core idea. The percent tells you how many dollars per hundred dollars per period. A 6% annual rate on a $10,000 loan means the lender charges $6 for every $100 borrowed each year, or $600 total for one year on the full amount.

Here is a quick way to state it: the interest rate is the price of using money, expressed as a percent of the amount, for a specific length of time. Whether you are earning it or paying it, the meaning is the same.

Let's apply everything we have covered to a real-world style statement:

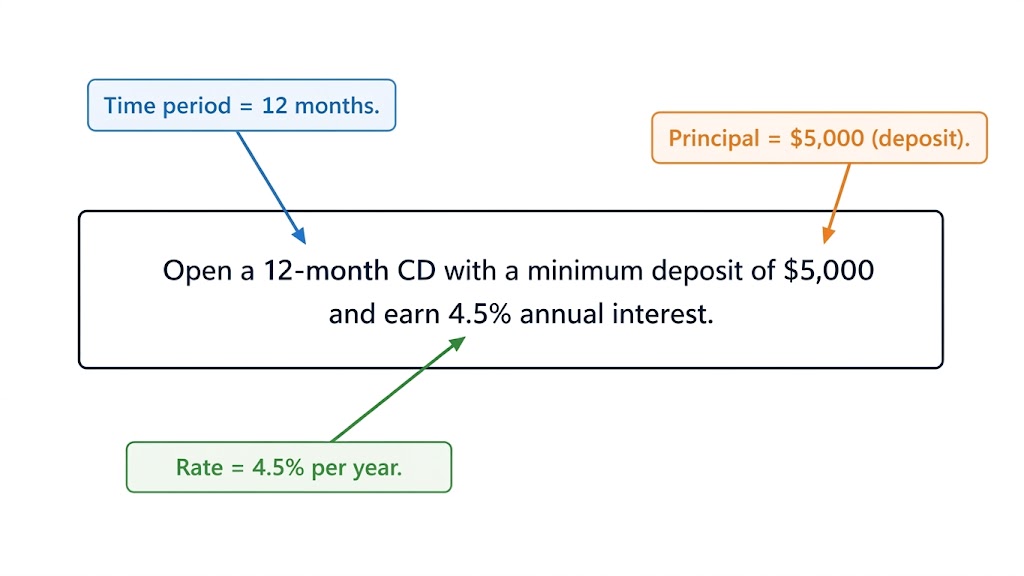

"Open a 12-month CD with a minimum deposit of $5,000 and earn 4.5% annual interest."

A visual breakdown looks like this:

We can pull out each piece:

- Principal: $5,000 (the deposit)

- Rate: 4.5% per year (annual interest)

- Time period: 12 months (the CD's term)

Notice that the rate says "annual" and the term says "12 months." Since 12 months equals 1 year, the rate and time period already match. In future lessons, we will use all three pieces to calculate exactly how much interest is earned or owed.

In this lesson, we learned that every interest situation comes down to three components: the principal (how much money), the rate (what percent per period), and the time period (how long). We also practiced spotting each one in realistic financial statements and put the meaning of an interest rate into plain language. These three components are the foundation for everything else in this course.

Up next, you will get to practice identifying principal, rate, and time period in a variety of savings, loan, and credit card statements on your own. This is a great chance to sharpen your eye for reading financial details before we start crunching numbers in the lessons ahead!